Ticker: SOFI | Exchange: NASDAQ | Sector: Fintech / Digital Banking | Rating: HOLD — Upgrading to Accumulate at $15 to $16

Current Price: ~$15.00 to $15.50 as of June 5, 2026, down ~7.23% today | 12-Month Base Target: $22 to $35 | Bull Case Target: $31 to $40

Executive Summary

SoFi Technologies is one of the most closely watched fintech names on Wall Street in 2026, and for good reason. The company has engineered one of the fastest financial turnarounds in digital banking history, growing from a loss-making student loan refinancer into a fully chartered national bank generating $1.10 billion in a single quarter of revenue, $166 million in quarterly net income, and 14.7 million members growing at 35 percent annually.

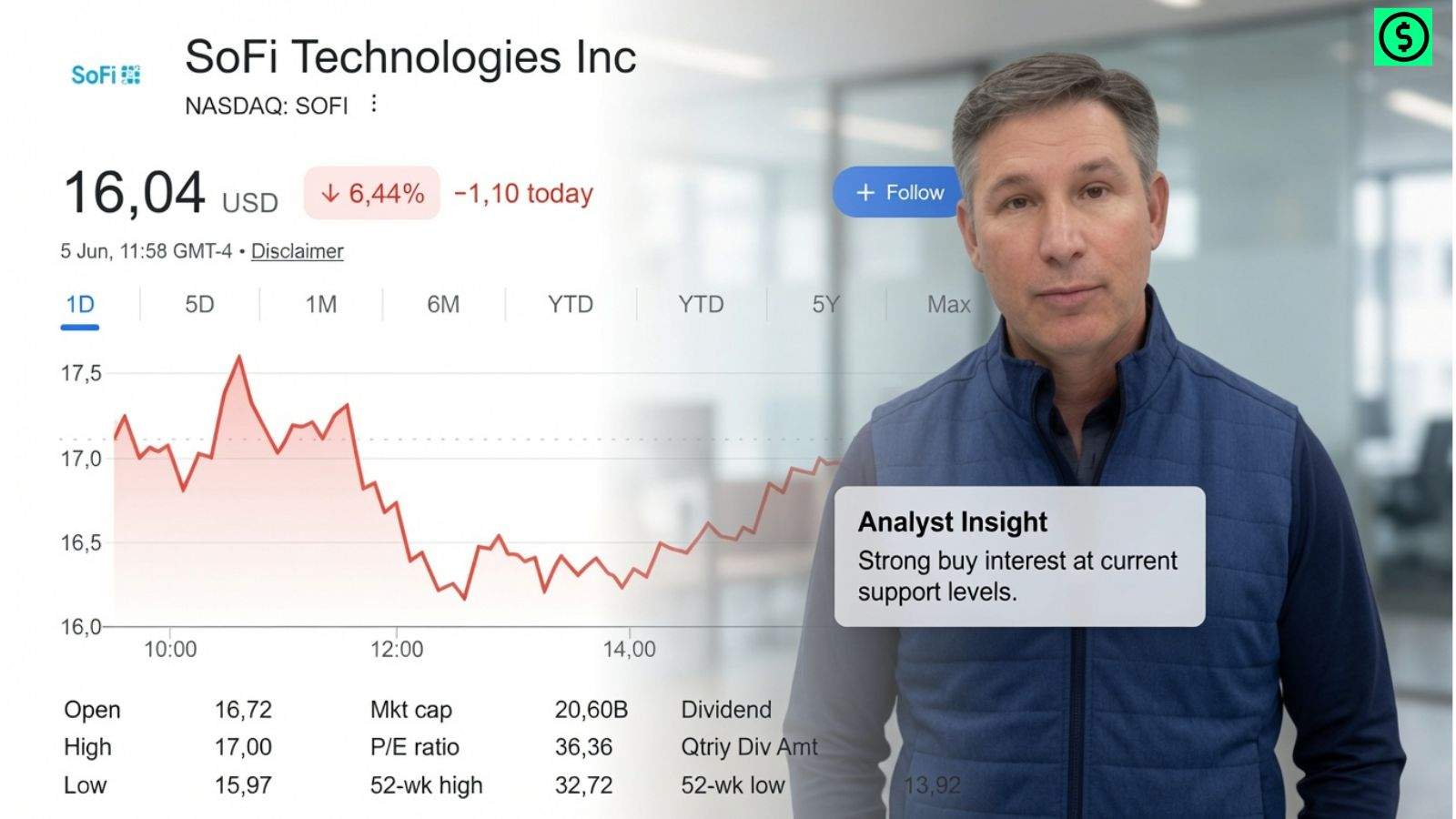

Today, June 5, 2026, the stock is down approximately 7.23 percent, trading in the mid $15 range, following a stronger-than-expected May jobs report that sent Treasury yields sharply higher across the curve.

I want to be direct with you from the start. Today’s selloff is not a story about SoFi’s business deteriorating. It is a macro rate shock story that has hit the entire financial sector simultaneously. My job in this report is to separate that noise from the signal, give you the most current data available, show you exactly what institutional investors and the biggest players on Wall Street are doing right now, and present a clear-eyed scenario framework so you can make an informed decision about where SOFI fits in your portfolio.

What Is Happening With SOFI Stock Today

The Macro Trigger Behind the 7% Drop

SOFI entered June 5, 2026 under pressure, and this morning’s May jobs report delivered the final blow. The report showed stronger-than-expected payroll additions and wage growth, which immediately caused bond markets to reprice Federal Reserve expectations. The 10-year Treasury yield climbed above 4.5 percent and the 30-year Treasury yield surpassed 5 percent in intraday trading.

For a lending-heavy financial technology company like SoFi, this creates two direct problems. First, net interest margin compression risk increases when rates stay higher for longer and deposit competition intensifies. Second, the equity risk premium embedded in growth-oriented financial stocks gets repriced upward, compressing the forward earnings multiple that investors are willing to pay. The same dynamic hit Fiserv, MarketAxess, and other financial services companies today. SOFI is not uniquely broken. It is uniquely exposed to the rate narrative because of its premium valuation relative to pure banking peers.

Where SOFI Stands Right Now

| Metric | Value | As Of |

|---|---|---|

| Current Share Price | ~$15.00 to $15.50 | June 5, 2026 |

| Today’s Move | Down ~7.23% | June 5, 2026 |

| 52-Week High | $32.73 | Late 2025 |

| Decline From 52-Week High | ~52% to ~54% | June 5, 2026 |

| Market Capitalization | ~$15B to $16B | June 5, 2026 |

| Median Analyst Price Target | ~$20.50 | June 2026 |

| Forward P/E on FY2026 EPS Guidance | ~25x to 26x | June 5, 2026 |

| Key Support Zone Watched by Traders | $15.00 to $16.00 | June 5, 2026 |

| Next Major Earnings Catalyst | Q2 2026 Earnings | July 28, 2026 |

At $15 to $15.50, SOFI is now trading at approximately 25 to 26 times forward earnings on FY2026 consensus EPS of $0.60. Two weeks ago at $18, that multiple was 30 to 31 times. The compression in price has meaningfully improved the entry point, and I will explain exactly what that means for your risk/reward later in this report.

The Real Reasons SOFI Has Fallen Over 50% From Its Peak

The Valuation Got Dangerously Stretched in Late 2025

When SOFI hit its 52-week high of $32.73 in late 2025, it was trading at approximately 50 to 55 times forward earnings. Let me put that in perspective for you. JPMorgan, the most profitable bank in American history, trades at 12 to 13 times forward earnings. Even the most aggressively valued high-growth regional banks rarely command more than 20 times. At 50 to 55 times, SOFI was priced for absolute perfection across every segment, every quarter, indefinitely.

When perfection does not arrive on schedule, stocks like that do not correct 10 percent. They correct 50 percent. I have watched this exact pattern play out across fintech names repeatedly. It happened with PayPal from its 2021 peak above $300. It happened with Upstart when it fell from $400 to under $20. The mechanism is always the same. Euphoria arrives, price discovery fails, and then a brutal re-rating brings the stock back toward fundamental fair value. SOFI’s business did not deteriorate materially. Its multiple did. That distinction is everything when you are trying to determine whether this is a buying opportunity or a value trap.

Chime Departing Galileo Destroyed the Premium Tech Narrative

In late 2025, Chime, one of Galileo’s largest clients, departed the platform. That single client departure caused Technology Platform revenue to collapse 27 percent year over year in Q1 2026. This mattered enormously to institutional investors because the premium bull thesis on SOFI was never just “growing lender.” It was “fintech infrastructure powerhouse with durable, recurring enterprise technology revenue.” When you lose the infrastructure story, you lose the justification for a technology-company multiple on what remains substantially a lending business. Wall Street repriced that judgment fast and hard.

The Muddy Waters Short Report Created a Sentiment Ceiling

In early 2026, Muddy Waters Research, the same firm that exposed Luckin Coffee and other corporate governance failures, published a critical report questioning SOFI’s earnings quality, loan classification practices, and certain revenue recognition approaches. SoFi management pushed back strongly and most independent sell-side analysts sided with the company’s response. However, Muddy Waters reports create what I call a sentiment ceiling even when the bear thesis is ultimately wrong. The cloud of doubt keeps institutional buyers cautious and keeps short sellers emboldened long after the initial report fades from headlines.

One data point from the report that I do take seriously is the normalized charge-off figure. When you strip out the effect of selling delinquent loans just before quarter-end, some analysts estimate the true personal loan charge-off rate is closer to 4.4 percent rather than the reported 3.03 percent in Q1 2026. That is not fraud. But it is a nuance that deserves more transparency from management, and I will want to see clarity on this point in the Q2 2026 earnings call on July 28.

The December 2025 Capital Raise Added Dilution Overhang

In December 2025, SoFi raised $1.5 billion in new equity capital. This was a strategically sound decision to fund loan origination capacity and the Big Business Banking platform build. But it also diluted existing shareholders at a time when the stock was near its highs, and combined with convertible notes maturing in 2026 and 2029, it created a legitimate dilution overhang that has kept large institutional buyers from accumulating aggressively since.

Q1 2026 Financial Performance: The Business Itself Is Not the Problem

Income Statement Highlights

Let me show you the actual numbers because I think the gap between operating performance and stock price is the central tension every SOFI investor needs to understand right now.

| Metric | Q1 2026 | Q1 2025 | Year Over Year Change |

|---|---|---|---|

| GAAP Net Revenue | $1.10B | $770M | +43% |

| Adjusted Net Revenue | $1.09B | $771M | +41% |

| Net Income | $166.7M | $71.1M | +134% |

| Adjusted EBITDA | $340M | $210M | +62% |

| Adjusted EBITDA Margin | 31% | 27% | +4 percentage points |

| Diluted EPS GAAP | $0.12 | $0.06 | +100% |

| Total Members | 14.7M | 10.9M | +35% |

| Total Products | 20.1M | 14.9M | +35% |

| Loan Originations | $12.2B | $7.3B | +68% |

| Total Deposits | $40.2B | ~$28B | ~+43% |

| Net Interest Margin | 5.94% | 5.98% | -4 basis points |

| Personal Loan NCO Rate | 3.03% | 3.31% | -28 basis points |

Full Year 2025 vs 2024 Comparison

| Metric | FY2025 | FY2024 | Year Over Year Change |

|---|---|---|---|

| Total Revenue | $3.6B | $2.6B | +35.6% |

| Net Income | $481M | $480M | +0.5% |

| Adjusted EBITDA | $1.1B | ~$750M | ~+47% |

| Diluted EPS | $0.42 | ~$0.08 | +425% |

FY2026 Management Guidance

| Metric | FY2026 Guidance | Implied Growth vs FY2025 |

|---|---|---|

| Adjusted Net Revenue | ~$4.655B | ~30% |

| Adjusted EBITDA | ~$1.6B | ~45% |

| Adjusted EBITDA Margin | ~34% | +4 percentage points |

| Adjusted Net Income | ~$825M | ~72% |

| Adjusted EPS | ~$0.60 | ~43% |

| Member Growth | At least +30% year over year | 14.7M to 19M+ |

A company guiding for $825 million in full year net income and $4.655 billion in adjusted revenue does not warrant a 52 percent stock decline based on fundamentals alone. This stock fell because of valuation excess, macro headwinds, and a technology segment disruption, not because the underlying business broke. Understanding that distinction is the foundation of any intelligent analysis of SOFI at current prices.

SoFi’s Competitive Moat: Why This Is Not Just Another Neobank

The National Bank Charter Advantage

In January 2022, SoFi received a national bank charter from the Office of the Comptroller of the Currency. This is the single most important structural fact about the company that most retail investors underweight in their analysis. Having a bank charter means SoFi can hold customer deposits directly, fund its own loan portfolio at wholesale cost, and offer FDIC-insured products without paying fees to a partner bank intermediary.

Competitors like Chime and Dave technically operate as technology companies layered on top of partner banks such as The Bancorp Bank or Stride Bank. They pay those banks a percentage of every transaction and are constrained by their partner’s balance sheet and regulatory posture. SoFi operates the entire banking stack itself. That creates structurally superior unit economics, greater product flexibility, and a regulatory moat that very few fintech startups have the capital, track record, or organizational capacity to replicate.

What the Bank Charter Means for SoFi’s Deposit Economics

As of Q1 2026, SoFi holds $40.2 billion in deposits, up approximately 43 percent year over year. Those deposits fund personal loans, student refinancing, and home loans at a net interest margin of 5.94 percent. Traditional banks with their sprawling branch networks and legacy overhead structures pay significantly more per dollar of deposit held. SoFi’s branchless model is the structural efficiency that allows them to simultaneously offer members 4 percent APY on savings balances while still generating nearly 6 percent NIM. Most traditional banks cannot match either rate because their cost structures prevent it.

The Galileo and Technisys Infrastructure Moat

SoFi acquired Galileo Financial Technologies in 2020 for approximately $1.2 billion and Technisys in 2022 to build out its Technology Platform division. Together, Galileo and Technisys power approximately 160 million enabled accounts across the broader fintech ecosystem. Galileo is the API-first payment processing and card-issuing infrastructure layer that allows other financial technology companies to build products without starting from scratch. Technisys is a cloud-native core banking system.

Yes, losing Chime hurt significantly. Yes, Q1 2026 Technology Platform revenue fell 27 percent year over year. But management has guided 13 new enterprise clients to ramp revenue throughout 2026, and the Technisys core banking platform is currently being deployed internally at SoFi Bank itself, with completion expected this summer. That internal live deployment is critically important: it transforms Technisys from a product being sold to third parties into a product that SoFi uses in its own regulated bank environment. In enterprise technology sales, a live reference customer in a nationally chartered bank carries more persuasive power than any marketing campaign.

The Member Flywheel and Cross-Sell Economics

| Period | Net New Members | Total Members |

|---|---|---|

| Q1 2025 | 800,000 | 10.9M |

| Full Year 2025 | 3.2M+ | 14.7M at start of Q2 2026 |

| Q1 2026 (record quarter) | 1.055M | 14.7M |

| Full Year 2026 Target | 4.3M+ | 19M+ |

The metric I monitor most closely beyond total member count is products per member, which currently sits at approximately 1.37 across the base. SoFi’s core business strategy is to acquire a member through a single entry product, most commonly the high-yield SoFi Money savings account or a student loan refinancing application, and then cross-sell that member into five or six additional products over a three to five year relationship. Each additional product adopted by a member dramatically improves their lifetime value while simultaneously reducing the marginal cost of acquisition across the overall member base.

CEO Anthony Noto has publicly stated that SoFi Gold subscribers, who pay a monthly premium fee for enhanced benefits and higher APY rates, exhibit significantly higher product adoption rates and engagement metrics than the general membership base. Premium membership tier adoption is one of the most reliable leading indicators of genuine platform stickiness in consumer finance. When users pay to stay, they are not leaving.

What the Biggest Players on Wall Street Are Actually Doing

Institutional Positioning and Analyst Consensus

While retail sentiment has turned sharply negative on SOFI and today’s macro-driven selloff has pushed the stock to multi-month lows, institutional behavior tells a more nuanced story. Smart money does not always follow the same narrative as financial social media.

| Analyst / Firm | Rating | Price Target | Date |

|---|---|---|---|

| JPMorgan | Overweight (Buy) | $31 | February 2026 |

| Citigroup | Bullish | $30 | May 2026 |

| Needham | Buy | $25 | April 2026 |

| Citizens | Upgrade | N/A | Early 2026 |

| Truist Securities | Hold | $17 (lowered from $20) | May 2026 |

| Bank of America | Underperform | $20 | Ongoing 2026 |

| Consensus Median Target | Mixed | ~$20.50 | June 2026 |

| Total Analysts Covering | 24 | 8 Buy / 11 Hold / 5 Sell | June 2026 |

Even at today’s depressed price of $15 to $15.50, the median analyst price target of $20.50 implies 32 to 37 percent upside. The most bullish institutional targets of $30 to $31 imply nearly 100 percent upside from current levels. Wall Street has not given up on this stock. What exists is genuine disagreement about whether SoFi’s premium multiple is justified at its current stage of development, and today’s macro shock has widened that debate.

CEO Anthony Noto: Putting His Own Money Where His Mouth Is

This is the data point I keep coming back to. On March 2, 2026, CEO Anthony Noto purchased 56,000 shares of SOFI at approximately $17.88 per share, spending roughly one million dollars of his own personal capital to buy stock near what were then multi-year lows. His total direct shareholding now stands at over 11.6 million shares. The stock today is trading at $15 to $15.50, meaningfully below the price Noto paid with his own money just three months ago.

Executives of Noto’s caliber, with his Goldman Sachs investment banking background and Twitter CFO tenure, do not spend seven figures of personal capital on a company they believe is in structural decline. They have access to information that public investors do not. They know the receivables quality, the pipeline, the client conversations, and the internal operating trends. Noto bought at $17.88. The stock is now cheaper.

The Short Squeeze Setup: Why July 28 Could Be Violent

Elevated short interest, estimated in the 10 to 15 percent of float range, combined with a business generating $166 million in quarterly net income, creates a textbook coiled spring dynamic. If Q2 2026 earnings on July 28, 2026 come in ahead of expectations, the forced short covering could amplify upside significantly beyond what the fundamental improvement alone would justify. I have observed this exact setup play out in PayPal in early 2023, in Block in late 2023, and in several regional bank names during rate-driven selloffs. When sentiment is this negative and short interest is this elevated against a profitable, growing business, the reversal, when it comes, tends to be fast and outsized.

SoFi’s Emerging Growth Vectors Not Yet in Any Earnings Model

SoFiUSD: The Stablecoin That Changes the Fee Revenue Story

In early 2026, SoFi launched SoFiUSD, a fully reserved US dollar stablecoin issued directly by its nationally chartered bank, designed to settle natively across the Mastercard payment network. I want to be careful here because I do not want to overstate what is still an early-stage product. But I also do not want to understate the structural significance.

SoFi is one of the very few nationally chartered banks in the United States that has issued a stablecoin at institutional scale. The combination of SoFi’s Federal Reserve master account, its FedNow real-time payment integration, and the Mastercard merchant acceptance network creates a settlement stack that most traditional banks will not be able to replicate for years. Revenue from SoFiUSD transaction fees and custody services is not yet material in any earnings model. But the positioning today is the revenue in 2028 and 2029, and I think the market is completely ignoring it.

Big Business Banking and the Enterprise Deposit Opportunity

On April 2, 2026, SoFi launched Big Business Banking, and the small and medium business banking rollout is underway in June 2026. This enterprise platform allows businesses, fintechs, and corporate treasury teams to hold deposits, execute payments, and settle transactions around the clock in both traditional dollars and digital assets. The platform runs on SoFi’s Federal Reserve master account and FedNow integration, giving it real-time settlement capabilities that most commercial banks do not offer outside of business hours.

Why Enterprise Deposits Are Fundamentally Different From Retail Deposits

Enterprise deposits are structurally superior to retail deposits in three ways. They are larger per relationship, reducing the per-dollar cost of acquisition and servicing. They are stickier because corporate treasury teams face significant operational friction when switching banking relationships. And they come with processing and custody fee revenue that retail deposit relationships do not generate. If SoFi captures even a modest fraction of the commercial and SMB deposit market, it restructures their funding economics favorably for years.

Management expects meaningful Big Business Banking revenue contribution by H2 2026, with a fuller commercial ramp expected throughout 2027.

The PrimaryBid Acquisition and IPO Access

In May 2026, SoFi agreed to acquire most assets of PrimaryBid, a fintech that democratizes retail investor access to IPOs and equity capital markets offerings. Historically, access to IPO allocations at the offering price has been gated exclusively to institutional investors and high-net-worth private wealth management clients. SoFi Invest members gaining genuine IPO access at offering prices is a product feature that no major retail brokerage currently offers at scale. This acquisition pushes SoFi directly into wealth management territory and competes on product depth with Schwab, Fidelity, and Robinhood in a way that meaningfully increases the lifetime value of each brokerage member.

S&P 500 Index Inclusion: The Forced Buying Catalyst

SoFi has now delivered nine consecutive quarters of GAAP profitability through Q1 2026. Its market capitalization sits at approximately $15 to $16 billion as of today. Several analysts I follow closely have quietly noted that SoFi is approaching S&P 500 index eligibility criteria. The requirements include sustained GAAP profitability, sufficient market capitalization, and adequate share liquidity, all of which SoFi now meets or is approaching.

S&P 500 index inclusion triggers automatic, non-discretionary buying from every index fund and ETF tracking the benchmark. That is trillions of dollars in assets required to hold the stock regardless of valuation. Historically, S&P 500 inclusion announcements have produced 5 to 15 percent price appreciation in the surrounding weeks. Beyond the mechanical buying effect, inclusion also signals to large institutional investors that a company has graduated from speculative growth to established financial institution, which often re-rates the multiple category the stock is placed in.

Risk Analysis: What Could Go Wrong

Comprehensive Risk Assessment

| Risk Factor | Probability | Impact | Current Mitigation |

|---|---|---|---|

| Technology Platform recovery stalls below $325M guide | Medium | High | 13 new clients ramping; Technisys enterprise pipeline building |

| Personal loan NCO rate rises above 4.5% | Medium | High | Prime FICO 749 borrower base; Loan Platform Business reduces balance sheet exposure |

| Treasury yields stay elevated, NIM compresses | Medium to High | Medium | Loan Platform Business fee revenue buffers rate sensitivity; Financial Services diversification |

| Valuation multiple compression continues | Medium | Medium | 52% decline from peak already a significant correction; CEO insider buying provides psychological floor |

| Normalized charge-off rate transparency risk | Low to Medium | Medium | Management has disputed Muddy Waters findings; independent analysts broadly constructive |

| Convertible note dilution in 2026 and 2029 | Medium | Medium | December 2025 $1.5B capital raise partially pre-funded near-term obligations |

| Regulatory or OCC compliance risk | Low | High | Bank charter well-established since 2022; constructive regulatory engagement history |

| Macro recession accelerating credit losses | Low to Medium | High | Stress-tested prime borrower portfolio; LPB model reduces held balance sheet exposure |

Credit Quality: The Risk I Am Watching Most Closely

Despite SoFi’s prime borrower focus, with an average origination FICO score of 749 in FY2025, credit quality deserves serious ongoing attention. Personal loan net charge-offs came in at 3.03 percent in Q1 2026, an improvement from 3.31 percent in Q1 2025 and from 2.80 percent in Q4 2025. That improvement trend is encouraging.

However, the normalized charge-off question raised by the Muddy Waters report, suggesting the adjusted rate may be closer to 4.4 percent when loan sales before quarter-end are excluded, has not been fully resolved by management’s response. In a recessionary scenario or a sustained high-rate environment, a charge-off rate above 4.5 percent would trigger meaningful provision expense increases and compress lending margins materially. This is the single risk I am most focused on, and I intend to track it closely through the Q2 2026 earnings call.

Interest Rate Sensitivity After Today’s Jobs Report

Today’s jobs report shock makes the rate sensitivity risk more salient than it was yesterday. SOFI’s FY2026 guidance explicitly assumed no Federal Reserve rate cuts in 2026. The market is now pricing in a non-trivial probability of rate increases before year-end. If that scenario materializes, three things happen to SOFI. NIM compresses as deposit rates stay competitive. Home loan originations, which are the most rate-sensitive category, slow. And the equity multiple gets compressed further as the discount rate applied to future earnings rises. The Loan Platform Business model, which earns origination and servicing fees without holding loans on the balance sheet, provides a meaningful structural buffer against this scenario but does not fully insulate SOFI from it.

Valuation Framework and Scenario Analysis

How I Approach Valuing SOFI

Valuing SoFi Technologies requires intellectual honesty about what kind of business it actually is. At 51 percent of revenue from Lending in 2025, it is substantially a bank. At 31 percent and growing from Financial Services and Technology Platform combined, it has genuine fintech characteristics. The appropriate multiple therefore sits between pure bank valuations of 12 to 15 times forward earnings and pure technology fintech valuations of 40 to 50 times. My fair value multiple range is 25 to 35 times forward earnings depending on execution quality, credit performance, and the Technology Platform recovery trajectory.

Bull Case: $31 to $40 by Mid-2027

| Factor | Bull Case Assumption |

|---|---|

| FY2026 Adjusted EPS | $0.65 to $0.70 (guidance beat) |

| Technology Platform | Returns to positive year over year growth by Q3 2026 |

| Big Business Banking | $50M to $100M incremental revenue contribution in 2027 |

| Personal Loan NCO Rate | Stabilizes at 2.8% to 3.0% |

| Member Base by End 2027 | 22M to 24M |

| S&P 500 Inclusion | Triggers forced institutional buying event |

| FY2027 EPS Estimate | $0.90 to $1.00 |

| Valuation Multiple Applied | 35x to 40x |

| Implied Price Target | $31 to $40 |

| Probability Estimate | 25% to 30% |

At today’s price of $15 to $15.50, the bull case implies 100 to 160 percent upside over an 18-month horizon.

Base Case: $22 to $27 by Mid-2027

| Factor | Base Case Assumption |

|---|---|

| FY2026 Adjusted EPS | ~$0.60 (in line with guidance) |

| Technology Platform | Modest H2 2026 recovery toward $325M full year guide |

| Financial Services Growth | 35% to 40% |

| Member Base by End 2026 | 19M to 20M |

| FY2027 EPS Estimate | $0.80 to $0.85 |

| Valuation Multiple Applied | 28x to 32x |

| Implied Price Target | $22 to $27 |

| Probability Estimate | 45% to 50% |

At today’s price of $15 to $15.50, the base case implies 42 to 74 percent upside over an 18-month horizon. This is meaningfully more attractive than the 20 to 50 percent upside the base case offered at $18 two weeks ago.

Bear Case: $10 to $14 by Mid-2027

| Factor | Bear Case Assumption |

|---|---|

| FY2026 Adjusted EPS | $0.40 to $0.50 (guidance miss) |

| Personal Loan NCO Rate | Rises above 4.5%, triggering provision increases |

| Member Growth | Slows to 20% to 25% due to macro headwinds |

| FY2026 Guidance | SoFi cuts guidance midyear |

| FY2027 EPS Estimate | $0.55 to $0.65 |

| Valuation Multiple Applied | 20x to 25x |

| Implied Price Target | $10 to $14 |

| Probability Estimate | 20% to 25% |

The bear case downside from today’s $15 to $15.50 price is approximately 7 to 33 percent. The base case upside is 42 to 74 percent. The bull case upside is 100 to 160 percent. That asymmetry has become substantially more favorable at today’s entry point than it was at any price above $18.

What I Am Watching on July 28, 2026

Q2 2026 Earnings Catalyst Checklist

July 28, 2026 is the single most important near-term date for every SOFI investor. Here is my precise checklist of what I need to see.

| Metric to Watch | Why It Matters | Threshold That Changes My View |

|---|---|---|

| Technology Platform Revenue | Must show sequential improvement toward $325M full year guide | Below $85M quarterly signals recovery is stalling materially |

| Personal Loan NCO Rate | Continued improvement validates credit quality narrative | Above 3.5% raises concern; above 4.0% is a material negative |

| Big Business Banking Disclosure | Any enterprise deposit wins de-risk the bull thesis significantly | Any named enterprise client wins are meaningful positive catalysts |

| Net New Member Count | Must maintain 1M+ quarterly pace established in Q1 | Below 900K suggests the member flywheel is losing momentum |

| FY2026 Guidance Status | Maintained or raised guidance is essential to sustain momentum | Any downward revision is a near-term significant negative |

| Management NIM Guidance | How does management frame NIM outlook after today’s yield spike | Forward NIM guidance below 5.5% would be a meaningful concern |

| Normalized Charge-Off Clarity | Management transparency on adjusted NCO methodology | Continued avoidance of this question extends the sentiment overhang |

Full Key Metrics Reference

| Metric | Value | Period |

|---|---|---|

| Current Share Price | ~$15.00 to $15.50 | June 5, 2026 |

| Today’s Price Change | Down ~7.23% | June 5, 2026 |

| 52-Week High | $32.73 | Late 2025 |

| Decline From All-Time High | ~52% to ~54% | June 5, 2026 |

| Total Members | 14.7M | Q1 2026 |

| Year Over Year Member Growth | 35% | Q1 2026 |

| Total Financial Products | 20.1M | Q1 2026 |

| Products per Member | ~1.37 | Q1 2026 |

| Total Deposits | $40.2B | Q1 2026 |

| Net Interest Margin | 5.94% | Q1 2026 |

| Personal Loan NCO Rate | 3.03% | Q1 2026 |

| Average Origination FICO | 749 | FY2025 |

| Loan Originations | $12.2B | Q1 2026 |

| Adjusted Net Revenue | $1.09B | Q1 2026 |

| Adjusted EBITDA | $340M | Q1 2026 |

| Adjusted EBITDA Margin | 31% | Q1 2026 |

| Net Income | $166.7M | Q1 2026 |

| Diluted EPS | $0.12 | Q1 2026 |

| FY2025 Total Revenue | $3.6B | FY2025 |

| FY2025 Net Income | $481M | FY2025 |

| FY2026 Adjusted EPS Guidance | ~$0.60 | FY2026 Estimate |

| FY2026 Adjusted Revenue Guidance | ~$4.655B | FY2026 Estimate |

| Market Cap | ~$15B to $16B | June 5, 2026 |

| Forward P/E on FY2026E EPS | ~25x to 26x | June 5, 2026 |

| Median Analyst Price Target | ~$20.50 | June 2026 |

| JPMorgan Target | $31 > Overweight | February 2026 |

| Citigroup Target | $30 | May 2026 |

| Needham Target | $25 | April 2026 |

| Truist Target | $17 > downgraded | May 2026 |

| Galileo Enabled Accounts | ~160M | Q1 2026 |

| Technology Platform Revenue Guide | ~$325M | FY2026 Estimate |

| CEO Insider Purchase | 56,000 shares at $17.88 | March 2026 |

| Key Technical Support Zone | $15.00 to $16.00 | June 2026 |

| Next Earnings Date | Q2 2026 | July 28, 2026 |

Investment Conclusion

My Verdict as of June 5, 2026

Here is exactly where I stand with SOFI at $15 to $15.50 and down 7 percent on the day.

The business is not broken. This is the most important thing I can say in this report. The company posted $1.10 billion in quarterly revenue, $166 million in quarterly net income, and is guiding for $825 million in full year net income for 2026. It is adding over one million members per quarter. Its deposit base of $40.2 billion is growing at 43 percent annually. The CEO purchased one million dollars of personal shares at $17.88 just three months ago, and the stock is now cheaper than when he bought.

Today’s selloff is driven entirely by a macro shock from the May jobs report, not by anything SoFi did wrong operationally. When fundamentally strong, profitable, rapidly growing companies sell off for macro reasons that have nothing to do with their business model, that is historically where durable investment opportunities are constructed.

Two weeks ago at $18, I rated SOFI a HOLD. At $15 to $15.50 today, I am upgrading my posture to HOLD with active accumulation at the $15 to $16 support zone. The base case scenario from current levels implies 42 to 74 percent upside through mid-2027. The bull case implies 100 to 160 percent upside. The bear case downside from today’s price is approximately 7 to 33 percent. For investors with a 24 to 36 month time horizon and the discipline to hold through quarterly volatility, this is the entry point you have been waiting for since the stock was at $32.

I will be providing a full update on July 28, 2026, the Q2 2026 earnings date, with a live reassessment of all key metrics and guidance assumptions. Follow investments-research.com and bookmark this page for that update.

Disclaimer: This article is produced for informational and educational purposes only and does not constitute investment advice, a solicitation, or a recommendation to buy or sell any security. investments-research.com and its contributors are not registered investment advisers. The information presented here is believed to be accurate as of June 5, 2026 but may be incomplete, subject to revision, or based on estimates. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. SoFi Technologies is a publicly traded company subject to significant market, credit, regulatory, and operational risks that may differ materially from those described in this report.